<<

5-Waters Volume 1

11 Financial Summary

This section outlines the financial projections and funding requirements for managing the 5Waters Activity for the next ten years. Managing and allocating funding determines the provision of infrastructure within the 5Waters Activity. This section also addresses the proposed change in rating, key assumptions made in this plan and asset insurance.

11.1 Financial Trends

Financial trends from the previous four years are shown below in Figure 11‑1, Figure 11‑2, Figure 11‑3, Figure 11‑4 and Figure 11‑5.

Figure 11‑1 Financial Summary for Water Supply Activity

Figure

11‑2 Financial Summary for Wastewater Activity

Figure 11‑3 Financial Summary for Stormwater Activity

Figure 11‑4 Financial Summary for Land Drainage Activity

Figure 11‑5 Financial Summary for Water Races Activity

These trends were used to forecast the financial projections for the next ten years. In these graphs the Operational Expenditure includes depreciation, support charges and operational projects.

11.2 Financial Statements and Projections

A high level summary of projects is provided in Section 3.0 Activity Areas, with financial summaries for each scheme presented in Volume 2-6 of this plan. The financial summaries presented should be viewed noting:

- Allowance for CPI – consumer price index adjustments 'inflation' has not been included; and

- All data is held in NCS – the Napier Computer Systems database through which Council conducts the majority of its financial rates storage and reporting.

The 10 Year financial programme for the 5Waters is divided into the following categories:

- Expenditure – Operations and Maintenance;

- Projects – either specific or jointly funded;

- Capital Projects - result in new assets; and

- Renewals - replacement of assets on a like for like basis within a 20 year horizon.

Across all of the 5waters the 10 year funding program for the next ten years is shown below in Figure 11‑6.

Figure 11‑6 Funding Program for 2018-2028

The remainder of this section details the financial projections across these four categories.

11.2.1 Expenditure

Expenditure consists of operational and maintenance costs. Figure 11‑7 shows the expenditure forecasted to maintain and operate the 5Waters schemes.

The majority of expenditure is reactive and scheduled maintenance undertaken in the under contract C1241 Water Services Networks Operations and Maintenance. Other expenditure includes electricity costs and consent application fees.

For the operations and maintenance costs, staff review the claim (consisting of water, water races, wastewater and stormwater activities) in AMS on a monthly basis. Claim items or “jobs" are accepted, or queried and amended before being accepted for payment. This enables staff to ensure that the contractor has provided all necessary information and data attributes. Land drainage is mostly managed outside of AMS and is not included under contract C1241.

Council's Corporate team also review the financial data on a quarterly basis. CPI adjustment is not provided in the financial data in this AcMP, though has been included in the Corporate groups forecasting.

Figure 11‑7 Funding Program - Expenditure

11.2.2 Projects

Projects are investigations, decisions and planning activities which exclude capital works. Projects are driven by growth, regulatory and Levels of Service demands. This includes applying for resource consents and running asset valuations via the AMS system. Each project is allocated to a year or years, with costs spread across applicable schemes who share jointly in the benefit of the work undertaken. Figure 11‑8 below details the projected spending for projects across the 5Waters for the next ten years.

Figure 11‑8 Funding Program – Projects

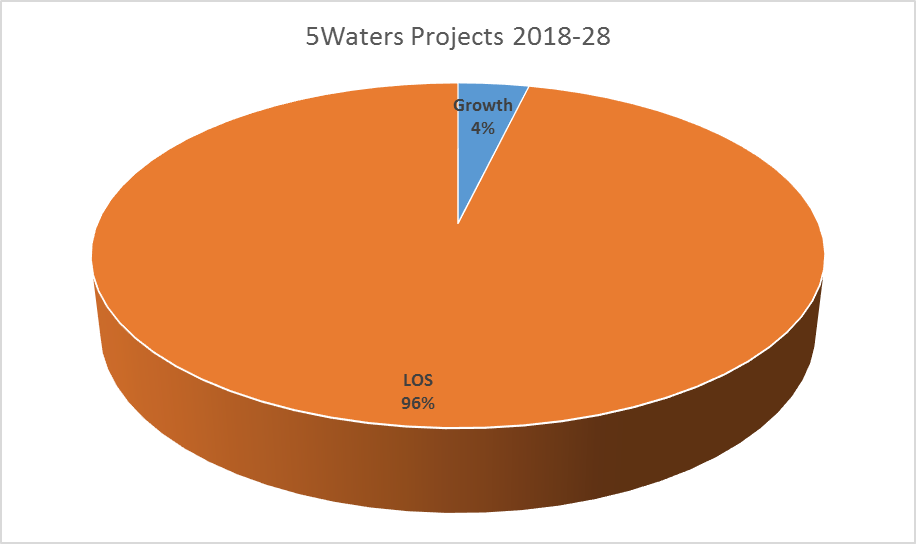

The split of level of service (LoS) verse Growth projects for the next ten years are shown below in Figure 11‑9.

Figure 11‑9 LoS and Growth Projects

11.2.3 Capital Projects

Capital projects are activities involving physical works. Capital works are divided into growth and levels of service categories. The basis for these capital works is robust. For example, installation of new Rolleston water wells is based on detailed water modelling (actual usage), BERL growth predictions and flow and pressure requirements. Works budgets are based on recent quotes for similar work, where applicable.

Capital levels of service works e.g. pipeline extensions (driven by development of subdivisions) and installing UV treatment (driven by increasing legislative requirements). Figure 11‑10 below details the projected spending for projects across the 5Waters for the next ten years.

Figure 11‑10 Funding Program – Capital Projects

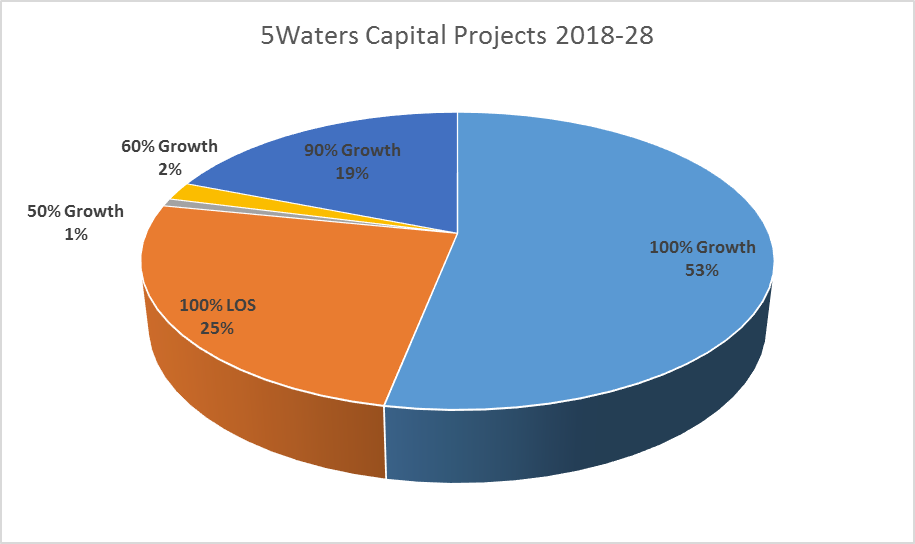

The split of level of service (LoS) verse Growth projects for the next ten years are shown below in Figure 11‑11.

Figure 11‑11 LoS and Growth Capital Projects

11.2.4 Renewals

Renewals are the replacement of assets which are nearing or exceeded their useful life as detailed in 7.8 Renewal Replacement Plan.

All schemes fund their renewal costs through their rates. This will provide sufficient funds for the proper upkeep of the assets. The total renewal costs expected to be incurred over the next 30 years (in line with the renewal program) will be funded on an even basis for this period. This approach will:

- Smooth out the generally uneven annual costs of renewals work;

- Ensure that Council can maintain the integrity of the scheme assets; and

- The scheme users now and in future generations will pay a fair charge that reflects the cost of operating and renewing the scheme over the next decade.

A renewals register has been developed on the back of the 2017 valuation process. A detailed review of assets was undertaken during this process – refer to 7.0 Lifecycle Management which details asset confidence, condition and valuation. It is appropriate to note that the value of the 5Waters assets are $ 0.60 billon. This has been developed and reviewed in conjunction with MWH. Annual depreciation or consumption of the asset is $7.3 million. This excludes open naturalised channels.

As the asset value increases, so does the renewals funding required to replace it. The level of funding for some communities for equipment and reticulation renewals in the next 5-30 years is a significant portion of the annual incomes for the individual schemes. A significant level of renewal works have been identified in 2022/2023. In 2022/23 the majority of these works consists of two components:

- Assets not renewed and carried forward from the 2015-25 LTP; and

- Assets that have a predicted renewal in the 2022-2023 period.

It is expected that assets in group i above will be, via further assessment, replaced within 5 years of the predicted renewal year. To ensure the most sustainable use of asset is achieved, Council staff will review the need for renewals based on the assets criticality, actual condition and any other relevant information. This includes a review of maintenance records. Table 11‑1 and Figure 11‑12 show the renewal profile for the next 30 years. This summary does not include non-depreciated assets, these asset types are listed in Section 7.5 Asset Valuations.

Table 11‑1 Renewal Profile 30 Years

| Land Drainage | 350,000 | 110,000 | 35,000 | | | |

| Wastewater | 8,463,888 | 9,423,357 | 4,902,225 | 5,126,007 | 1,089,770 | 3,102,018 |

| Stormwater | 317,801 | 233,645 | 51,866 | 215,814 | 1,868,131 | 1,472,240 |

| Urban Water | 11,795,997 | 8,277,724 | 7,051,041 | 6,379,315 | 2,247,069 | 2,383,186 |

| Water Races | 6,262,054 | 1,200,579 | 226,718 | 357,385 | 271,629 | |

|

Total | 27,189,740 | 19,245,305 | 12,266,851 | 12,078,520 | 5,476,598 | 6,957,444 |

Figure 11‑12 30 Year Renewals Summary

11.2.1.1 Depreciation

The base value of an asset reduces in accordance with the wearing out over the asset's life arising from use, the passage of time, or obsolescence.

Depreciation is a measure of how much of an assets value has been used up. For example, if an asset will last for 50 years, the annual depreciation charge is 1/50th of the value of the asset. The Council gets all land, building and infrastructure assets revalued every three years to ensure the value is a true reflection of the replacement cost of that asset. Accordingly, this means that the annual depreciation charge also reflects the replacement cost of the asset. It is the asset valuers role to appropriately identify the level of depreciation, though this will be better achieved through more robust data e.g. condition assessment.

Annual depreciation is calculated by Council on a straight line basis – i.e. the replacement cost of the asset less its residual value divided evenly over its useful life. The Council has previously consulted with the Community and decided not to fund depreciation via targeted rates for 5Waters activities. Council instead funds renewals expenditure.

This AcMP has been assembled on the basis that all schemes covered by the 5Waters undertake to fund their renewal costs through their rates. The total renewal costs expected to be incurred over the next 30 years will be funded on an even basis for this period resulting in a smoothing out the generally uneven annual costs of renewals work. This approach to renewals funding will mean the Council can maintain the integrity of the scheme assets and the scheme users will pay a charge that reflects the true cost of operating and renewing the scheme over the next decade.

11.3 Funding strategy

Provision of new infrastructure and operations and maintenance of existing assets is funded by a mixture of rates and development contributions. The funding strategy is outlined in the Revenue and Financing Policy.

Over the period of the 10 year plan, Council's intends to ensure the financial position is neutral at a minimum. This is a general rule, with recognition of particular renewals and capital works directing this position on a scheme by scheme basis.

11.3.1 Rating

11.3.1.1 Existing Rating System

A districtwide rate exists for water and wastewater services. This means that most people pay the same for these services, no matter where they live.

The approach to funding land drainage and water races is different as only those who benefit (directly or indirectly) pay, termed targeted rating.

The Councils financial year commences 1 July annually. Therefore any reference to 201#-201# is for a 12 month period 1 July to 30 June.

Presently the owners of properties that are connected to a:

- Public water supply pay a district wide rate based on either a flat rate and/or the amount of water they use.

- Wastewater scheme pay a district wide rate based on a flat rate.

- Water race scheme pay a targeted user charge and/or area rate and or irrigation rate as appropriate. Targeted rates vary from water race scheme to water race scheme.

- Land drainage scheme pay a targeted rate based on the level of benefit – via classification system.

- Stormwater scheme pay a district wide rate based on a serviced area.

In some areas where properties are capable of being connected but which are not connected, the owner pays an availability charge i.e. half rate in recognition of the benefits of being able to connect when they wish.

11.3.1.2 Proposed Rating System

The Council is proposing to introduce a new rating structure for the water race network, based on a standard district rate. There are currently three water race schemes within the district: Ellesmere, Malvern and Paparua. Over the past five years, however, substantial changes have been identified which are expected to change the need for and use of the schemes. The water races bring other benefits to the Selwyn community rather than just the traditional demand for water for livestock. A change in rating will ensure that land owners who benefit directly from access to water races still fund the majority of the costs, but that the wider community also contributes to the costs. Over time, as the traditional use of water races for farming declines, the wider community will pick up an increasing proportion of the costs.

The current rating structure for water races is complicated, with 10 different rating factors operating across the three networks. Water race rates are paid by rateable properties in each rating area where the service is available, and in addition some rural areas and townships pay a public good rate to reflect the broader benefit of water races. The proposed new rating structure provides three standardised rating factors to replace the existing 10 rating factors. The new structure is provided below.

Table 11‑2 Proposed Rating Structure

| Water race user | Annual change revenue

| $300 | 6.0%

|

| Water race user | Per hectare revenue | $17 | 6.0% |

| Al ratable properties | Public/environmental rate revenue | $20 | 10.0% |

The Council is proposing to review the rating structure of the Land Drainage activity during the period of this LTP. This is due to the increasing number of issues emerging for the land drainage schemes.

Figure 11‑13 below shows the predicted funding that will be received over the LTP period.

Figure 11‑13 Targeted Rates Revenue 2018-2028

11.3.1.3 Financial Affordability and Sustainability

Section 0 outlines the principle of financial sustainability. It states that in terms of asset management financial sustainability can be managed through:

- District wide rates;

- Integration of schemes; and

- Shared projects.

This section has already detailed the new proposal for a water race district wide rate which will help ensure financial sustainability and affordability.

Scheme integration was also discussed in Section 0. It stated that the Council has a number of smaller water schemes, although the continued growth within the district may enable some schemes to be joined together. This will lower the cost of providing services and ensure financial sustainability in the long term.

Scheme integration within the district to be investigated is:

- Connecting Edendale Water Supply to West Melton;

- Connecting the Johnson's and Jowers Road supplies to the West Melton supply; and

- Connecting some of the Darfield network to the Sheffield network.

The Branthwaite Drive water supply was integrated into the Rolleston scheme in late 2014. Armack Drive and Burnham water supply were connected to the Rolleston scheme in July 2015.

Shared projected are another way to share costs across a number of schemes who receive the benefit. As mentioned previously, examples of these projects are providing education, improving AMS functionality and running asset valuations. Often these projects are required as they relate to government regulation or enhancing processes. Jointly funded it shares the burden and enables a better solution.

11.3.2 Development Contributions

Territorial authorities may require contributions to the cost of infrastructural developments under the Local Government Act 2002 (the Act) and the Resource Management Act 1991 (the Resource Management Act).

The purpose of development contributions is to enable territorial authorities to recover from those persons undertaking development a fair, equitable, and proportionate portion of the total cost of capital expenditure necessary to service growth over the long term.

In determining whether development contributions are an appropriate funding source for different activities, the Council considers, for each of its activities:

- The community outcomes to which the activity primarily contributes;

- The distribution of benefits between the community as a whole, any identifiable part of the community, and individuals;

- The period in which benefits are expected to occur;

- The extent to which the actions or inaction of particular individuals or a group contribute to the need to undertake the activity; and

- The costs and benefits, including consequences for transparency and accountability, of funding the activity distinctly from other activities.

The Council then considers the overall impact of any allocation of liability for revenue needs on the current and future wellbeing of the community.

A development contribution is required in relation to a development when:

- The effect of that development requires the Council to construct new or additional assets for any network infrastructure, reserves or community infrastructure; and

- The Council has to incur capital expenditure to increase the capacity of existing assets (e.g. network infrastructure, reserves and community infrastructure) to support the growth from development.

The effect of development in terms of the impact on assets includes the cumulative effect that a development may have in combination with another development. A Development Contributions Policy also enables the Council to require a development contribution that is used to pay, in full or in part, for capital expenditure already incurred by the Council in anticipation of development.

The Council will not require a development contribution for network infrastructure, reserves or community infrastructure in the following cases:

- Where it has, under section 108(2)(a) of the Resource Management Act , imposed a condition on a resource consent requiring that a financial contribution be made in relation to the same development for the same purpose; or

- Where the developer will fund or otherwise provide for the same reserve, network infrastructure, or community facilities; or

- Where the territorial authority has received or will receive funding from a third party for the same purpose.

Where possible, capital works associated with maintaining levels of service (due to growth) or improving levels of service e.g. water quality, will be funded from development contributions. Further information can be in the Councils development contribution policy as required by section 102 (2)(d) of the Act, included in this LTP.

11.3.3 Capitalisation

Asset costs are initially recorded in the capital expenditure ledger, for the initial aggregation of costs and Annual Plan reporting. The balance in this ledger represents the amount of work in progress at any given time.

On a yearly basis, the value of completed assets or completed stages of major assets are transferred out of work in progress into the fixed asset register. The transfer is driven by the Certificate of Practical Completion and 224 Certificate in relation to subdivisions. The value of the assets is broken down into asset type.

Any significant subsequent expenditure after the initial recording of an asset can be capitalised under two conditions. These are if:

- It is probable that the expenditure will result in a higher Level of Service, or increase the useful life over the initial expected Level of Service or useful life; and

- The expenditure was necessary to obtain the previously expected Level of Service or useful life, and would have been considered part of the initial costs, but for the period of expenditure.

11.3.4 Vested Assets

The Council receives assets that are vested in it, but there has been no direct exchange of funds. In the case of infrastructural assets, the value of exchange is deemed to be at the current valuation at the time of issue of the 224 Certificate. For all donated and subsidised assets, the initial value recorded is the current valuation value at the date of acquisition.

For the period ended 30 June 2016 $17.17million in assets were vested to Selwyn District Council. A trend of vested assets is shown below by Figure 11‑14.

Figure 11‑14 Vested Assets 2011-2016

11.3.5 Future debt requirements

Council's policy on maintenance accounts is that operating accounts are allowed to be in deficit for 3 years with no interest charged.

From a borrowing position, Council has a debt ceiling of $130 million in 2018. Future revenue increases will raise this limit over the next 10 years. Current projects are that the Council will remain well within its limits over the next ten years. The ESSS exposes the council to some financial risk as funding of its finance costs is by way of development contribution, which is an uncertain revenue source. To mitigate this risk the Council has resolved that it will charge a targeted rate if required to offset any shortfalls. ESSS debt was at approximately $19 million at 30 June 2017.

11.4 Asset Insurance

The Council has insurance cover for the 5 Water services, property and staff as detailed in the Table 11‑3 below.

Pre the September 2010 earthquake, the Council was able to obtain insurance cover for “all perils" being fire, flood, earthquake and other natural disasters. This cover was in place until 30 June 2011, but cover for infrastructural assets could not be obtained during the period 1 July 2011 to 30 June 2014. Due to this lack of cover, the council instigated a risk management strategy where $10 million of its general funds cash was “ring fenced" for use as replacement funding of earthquake damaged underground assets. Since 1 July 2014 Council has obtained underground asset cover from a private insurer that provides a local share (40%) to a value of loss of $100 million with a further central government share (60%) to a value loss of $150 million being a total of $250 million. Council's underground assets were valued at $602 million as at 30 June 2017. The excess on the private policy is $5 million and the above mentioned cash reserve would fund this excess plus any excess on a claim against central government. The difference between the insured loss and total value of the assets recognises that when assets are damaged by earthquakes, there is only a remote possibility of total loss and thus the lower value of $250 million is an acceptable level of insurance cover.

Table 11‑3 5Waters insurance Provision

Reticulation

| | |

|

✓ |

✓ |

| Treatment Plants & Pump Stations | |

|

✓ |

✓ |

✓ |

| Electrical | | |

✓ |

✓ |

✓ |

| Mechanical | | |

✓

|

✓

|

✓ |

| Structural |

| | |

✓

|

✓ |

Staff

|

✓

|

✓ | | | |

| Council Vehicles | | | |

✓

| |

| Private property damage related to 5Waters damage |

✓

| | | | |

✓: Indicates coverage by that particular insurance type

(Note 1): There are a number of exclusions with this policy.

Insurance Process and Practices

All existing, new and vested assets have suitable insurance cover with all these assets held in the Councils AMS system. A valuation of these assets is undertaken 3-yearly with the revalued insurance values provided to Property and Commercial staff to amend the insurance cover.

On an annual basis insurance cover is automatically provided for all new assets constructed or vested in any one year without the Council insurer requiring notification. This automatic cover is provided on the basis that the insurer will be notified of the new assets as soon as practicable after the end of the financial year. With the end of financial year complete these new additions are provided to Councils Corporate Services for inclusion on the Council insurance register.

11.5 Key Assumptions

In 2017, Council adopted a set of assumptions for use during the preparation of AcMPs which underpinned the 2018-2028 LTP. This section outlines these assumptions. To ensure consistency across all activities, these assumptions have been prepared by an Activity Management Plan Steering Group for all infrastructural asset based activities. This section provides an update to the initial assumptions and related uncertainties tabled and discussed by the steering group in September 2017.

Table 11‑4 Significant Assumptions & Uncertainties for the Selwyn Long Term Plan 2018-2028

| All | Financial | Fees and charges | | Operational revenue is based on current service charges and, in the future, it is assumed charges for services will vary little from present day apart from inflation adjustments. | Low

| Fees will be insufficient to meet expenses | Council may review its existing fee structures and charging policy which would affect revenue streams. Adjustments can be made via the Annual Plan process.

|

| All | Financial | Investments | The Council | The funds may be invested externally or internally at the Council's cost of capital. | Low

| There is a risk that the Council will revise this policy and allocate these funds differently. | Should the Council allocate or retain these funds differently, there will inadequate funds for roading improvements, or the income available to support the general rate requirement will reduce and the Council may need to increase rates or reduce expenditure. |

| All | Financial | Renewal Funding & Programme | | 5Waters: A minimum 30 year renewal plan is followed, with funding via targeted scheme funding, general rates, and external sources as relevant to the asset. No depreciation funding occurring for any assets on the basis that actual identified renewal needs form the basis of ongoing funding needs. | Low | That renewal planning in inappropriate and there are funding consequences | Condition assessments and deterioration modelling of assets establish renewal needs and programmes. Current users may consume the assets but not contribute their share of the use they have made. Costs would then be carried by future users without the benefit having been received. |

| All | Financial | Renewal Funding & Programme | | Transportation: A minimum 10 year renewal plan with indicative renewal out to 30 years is followed, with funding via general rates, and external sources as relevant to the asset. It is noted that NZTA financial assistance is only allocated in three-year blocks. No depreciation funding identified for any assets on the basis that actual identified renewal needs form the basis of ongoing funding needs.

| Low | That renewal planning in inappropriate and there are funding consequences | Condition assessments and deterioration modelling of assets establish renewal needs and programmes. Current users may consume the assets but not contribute their share of the use they have made. Costs would then be carried by future users without the benefit having been received. |

| All | Financial | Renewal Funding & Programme | | Property: The renewals programme has been developed from condition assessments to component level for most asset groups. Remaining useful life has been calculated using standard industry lives and input will be sought from management committees where appropriate to refine programmes. It is assumed that this will provide a realistic renewals programme that ensures assets continue to deliver services to required standards. | Low | That renewal planning in inappropriate and there are funding consequences | Condition assessments and deterioration modelling of assets establish renewal needs and programmes. Current users may consume the assets but not contribute their share of the use they have made. Costs would then be carried by future users without the benefit having been received. |

| All | Financial | Resource consents | The Council | It is assumed that the conditions of Resource Consents held by the Council (requirements and costs) will remain similar to current levels, and that the Council will obtain the necessary Resource Consents for planned projects and ongoing needs in the future. | Moderate | There is a risk that the consent conditions will change or that consent will not be obtained for the Council projects. | If consent conditions change, expenditure may increase to comply with the conditions and this may have an impact on rate levels. If consents cannot be obtained for planned projects, the project may be delayed or may not go ahead. |

| All | Growth | Tourism | | That tourism numbers will increase at a similar rate to population growth and that facilities will be adequate | Moderate | That unexpected tourism growth will put pressure on facilities that was not anticipated | Facilities will be overused and/or pollution occurs |

| All | Lifecycle | Central Plains Irrigation Scheme | The Council | Following on from the successful completion of Stage 1 of the Central Plains Water Ltd Scheme supplying surface water to 23,000 Ha in the Te Pirata Area; Infrastructure is being constructed to irrigate 20,000 Ha in the Darfield area (Stage 2), and 4300 Ha in the Sheffield/Springfield area. | Moderate | There is a risk that the scheme proceeds more quickly or slowly than assumed | If the impacts of the establishment of the scheme are not understood then planning for ongoing use (or ease of use) will be incorrect. |

| All | Lifecycle | Data Quality and Management | | Investment in maintaining and developing the required level of quality data to efficiently operate and predict issues. | Low | Insufficient information leads to poor decisions | Incorrect data or inefficient or use of available data may result in relatively poor decisions on investments in operational, maintenance, renewal and capital, projects both in the short and long term. |

| All | Lifecycle | Major Project & Capital Works | | Will be estimated on the basis this work is facilitated by external consultants. Construction Projects costs estimated using the following:

a. Estimate +/- 25%

b. Where designed +/10%

c. Post tender +/-5% | Moderate | Project scoping and estimates are insufficient for budgeting purposes, or are excessive for potential projects | Conservative funding approach, staff may have capacity to undertake some work.

Particular skill sets in high demand may attract higher costs. |

| All | Lifecycle | New Technologies | | There will be no new technologies deployed that will

significantly change the demand for or of provision of services. | Low | Service delivery is poorly aligned with community demand | Inefficient of ineffective provision of services in the traditional manner when other alternatives maybe available. |

| All | Lifecycle | Planning Horizons | | It is assumed that the planning horizon for growth (30-45 years) and asset lifecycles (30 years plus) are sufficient to inform the ten year forecasts included in the LTP. | Low | Nil | Planning is less robust for long term decision making. |

| All | LoS | Iwi relationship | | Council will foster and positively develop its relationship with Iwi.

| Low | An ineffective relation causes misunderstandings and delays in planning and consent applications | A poor relationship may result in delays and additional costs in completing District Plan variations, Water Conservation Order matters and Structure Planning as delays and resources concentrated or within drawn at critical points in Councils work programmes. |

| All | LoS | Procurement of Services | | Procurement will be provided that delivers the defined LoS within budget, at a similar cost to that presently incurred in accordance with the Asset Procurement Strategy. | Moderate | Service providers cannot be secured and/or costs are greater than expected | A change in procurement model may result in unacceptable reduction in LoS. |

| All | LoS | Service delivery modes & contracts | | It is assumed that there will be no significant changes to current modes of service delivery for each service area or variations in terms of contract prices (above inflation and inventory adjustments) for current operations and maintenance contracts.

Council will continue to consider collaboration opportunities and assess changes to service delivery on a case by case basis. | Moderate | That service delivery modes do not demonstrated

value for money outcome. That changes to service delivery modes are enforced. | Maintenance contracts may be re-tendered during the plan period. If maintenance and service contracts are consolidated and/or re-tendered there is a possibility contract prices will be higher than anticipated. This would require Council to either increase rates and/or operating revenue if efficiencies cannot be found or it may consider reducing levels of service.

|

| All | LoS | Service Delivery | | That reviews of service delivery modes (LGA 2002 s17) will not initiate significant changes to service delivery modes

| Moderate | That service delivery modes do not demonstrated

value for money outcome. That changes to service delivery modes are enforced. | That there is a drive for a change in service delivery modes affecting management and providers |

| All | Sustaina-

bility | Gravel extraction potential | | It is assumed that sufficient gravel will be available for projects proposed. It is acknowledged that Council's Gravel Management Strategy proposes a wider range of sources than Council managed sites in future, this may be associated with a different cost structure. | Moderate | That there will inadequate supply from commercial or Council sources | If volumes of gravel available from various sources are considerably lower than anticipated, this may necessitate a greater reliance on Council or purchase of alternative sites or consideration of other supply sources/options. Consequently the cost of gravel supply would increase. |

5Waters Transpor- tation | Lifecycle | Asset Condition | | The condition and remaining typical life have been accurately assessed, permitting appropriate renewal forward programmes to be developed and routinely updated. | Moderate | Asset renewals are required earlier than expected | Earlier replacement of assets than forecast and budgeted. Scale of replacement will impact on funding that may produce funding peaks. |

5Waters Transpor- tation | Lifecycle | Asset lives | | Asset lives have been adopted from the best information available at the time of assessment.

Asset lives will not be modified due to the 2010 and 2011 earthquakes unless an assessment indicates otherwise. | Moderate | Asset renewals are required earlier than expected | Renewal cycles and associated Funding to support this may require change, generally this is seen as an increase in funding.

|

5Waters Transpor- tation | Sustaina-

bility | Criticality (consequence of failure) | | Staff will target resources based on the level of criticality and risk (highest to lowest where criticality has been assessed). | Low | Prioritisation is inappropriate | Consent non-compliance, enforcement cost, additional operational, maintenance and capital (remedial) works may result from incorrect assessments and targeting |

| 5Waters | Financial | Government Funding | | Our communities will not qualify for central government funding to improve sewer or water scheme works e.g. water quality upgrades. | Low | Nil | Schemes will have covered cost of improvements directly. |

| 5Waters | Financial | National Policy Statement on Freshwater Management | | It is assumed that any changes to the operation of Council's 5 Waters systems required by the implementation of the National Policy Statement on Freshwater Management can be addressed within existing budgets. | Moderate | There is a risk that the requirements will be greater than expected | Management and operational changes will be required to capital works and operations programmes as well, as the funding of these programmes. |

| 5Waters | Growth | Demand Management | | Demand management techniques will be applied and implemented as appropriate to networks, schemes and service areas both in the Council and user management areas. | Moderate | Consumption exceeds supply | 5Waters Consumption beyond current pipe capacity or consented quantities by existing users may mean additional connections will only be available at unreasonably higher cost. Efficiencies in scheme use may not be achieved; e.g. cost effective reduction in groundwater infiltration to sewer lines may not be possible. |

| 5Waters | Lifecycle | Stormwater Management (townships) | | Management Plans will be completed and consented in all townships.

That budgets will be sufficient for implementing the required actions | Moderate | Plans are not completed or consenting affecting compliance and overall planning success | Administration and monitoring of many small consents in townships will become more complex as development continues and NRRP/L&WP operative rules result in further resource (cost) increases. |

| 5Waters | LoS | Darfield / Kirwee Wastewater disposal | | There will be a clear community preference arising from the 2017/18 Annual Plan process | Moderate | That there will be no clear direction to pursue | That without a mandate, a decision to proceed or not proceed proves incorrect |

| 5Waters | LoS | Fluoridation | | That there will be no requirement imposed to floriate SDC Managed Water Supplies | Moderate | That fluoridation will be imposed on schemes along with the associated costs | Unbudgeted capital works and operations costs will result if fluoridation is required by the District Health Board |

| 5Waters | LoS | Havelock North Water Supply Enquiry | | That any additional actions arising from the Havelock North Water Enquiry can be accommodated with current management practices and budgets. | Moderate | That additional management actions will be imposed on schemes along with the associated costs | Unbudgeted capital works and operations costs will result if treatment or reticulation management process changes are required |

| 5Waters | LoS | Stormwater Levels of Service | | Community expectations for stormwater services across district township will increase over time, but there will be no urgent demand for extensive new networks and / or flood protection works within the first three years of the LTP | Moderate | That there will be a demand for services that exceeds allocated budgets | Unbudgeted capital works and operations costs will result |

| 5Waters | LoS | Chlorine treatment of water supplies | | Council will adopt a risk management approach for the assessment and use of chlorine treatment in its water supplies. | Moderate | That widespread chlorination will be required above the risk currently assessed. | Unbudgeted capital works and operations costs will result if treatment or reticulation management process changes are required |

| 5Waters | LoS | Upper Selwyn Huts Wastewater disposal | | There will be a clear community preference arising from the 2017/18 Annual Plan process | Moderate | That there will be no clear direction to pursue | That without a mandate, a decision to proceed or not proceed proves incorrect |

| 5Waters | Sustaina-

bility | Groundwater Source | | That groundwater nitrate levels will remain below the Maximum Acceptable Values (MAV) over the next ten years. | Low | The nitrate levels rise to a value that affects cost effect treatment of water supplies | That additional treatment will be required, affecting works programmes and expenditure required. Otherwise new sources mat be needed. |

| 5Waters | Sustaina-

bility | Groundwater Source | | Secure ground water status will be lost over the next ten years on bores located in semi aquifers and bored less than 30m deep in confined aquifers. | Moderate | That there will be a greater change to groundwater sources than expected. | That additional water sources will be required, affecting works programmes and expenditure required. |

11.6 Forecast Reliability and Confidence

The AcMP and financial projections are based on the best available data. Correct financial projections and accuracy of data is pivotal to effective asset and financial management. The same confidence grading as the asset valuation (shown in Table 11‑5 below), where data confidence is classified on a four tier scale, was used to determine a forecast reliability and confidence grade.

Table 11‑5 Data Confidence Grading

A

|

Highly Reliable Data based on sound records, procedure, investigations and analysis which is properly documented and recognised as the best method of assessment. |

B

|

Reliable Data based on sound records, procedure, investigations and analysis which is properly documented but has minor short comings; for example the data is old, some documentation is missing and reliance is placed on unconfirmed reports or some extrapolation and recognised as the best method of assessment.

|

C

|

Uncertain Data based on sound records, procedure, investigations and analysis which is incomplete or unsupported, or extrapolation from a limited sample for which grade A or B data is available. |

D

|

Very Uncertain Data based on unconfirmed verbal reports and/or cursory inspection and analysis |

The estimated confidence level and reliability of data used in this plan is shown in Table 11‑6 below.

Table 11‑6 Data Confidence Assessment for Data Used

Growth Projections

|

|

|

| |

| Based on projections from the planning department

|

Asset Value and Useful lives

|

|

| | |

| Sourced from 5Waters Valuation Report 2017

|

Condition Modelling

| | |

|

| Condition modelling only exists for pipes within the reticulation network

|

Demand and Capacity

|

|

| | |

| Based on outputs from water models run by Opus Consultants for major growth areas and desktop review for smaller schemes

|

Operations and Maintenance Budgets

|

|

| | |

| Based on C1241 pricing and previous trending |

Projects and Capital Projects Budgets

|

|

| |

| Based on consultant reports, engineer estimates and staff experience

|

Network renewals and renewal budgets

|

|

| |

|

| Sourced directly from the 2017 asset valuations |

Overall Confidence and reliability

|

|

| | |

|

|

Overall, the data confidence is assessed as a reliable confidence level for data used in the preparation of this AcMP.

Asset management issues that impact on the confidence have been identified for improvement throughout this AcMP. To improve the process of budgeting and forecasting going forward, it is suggesting that budgeting editing software could be used. This could be linked with NCS, therefore eliminating the manual checking of spreadsheets by asset management and the corporate team. This will also give the service delivery team a greater opportunity to input cost estimates for projects and suggest additional projects.

Compliance with GAAP

All Council activities are required to have their financial results reported externally in a way that complies with generally accepted accounting practice (GAAP) in New Zealand. This is currently in accordance with International Accounting Standards – IAS16. The International Accounting Standards are determined by the Institute of Chartered Accountants of New Zealand. The Finance Activity ensures that GAAP is complied with by regular updates to the Council's Accounting processes, and the on-going formal and informal training and education of staff in departments throughout the Council.

The activity relies on the Council's core financial systems which include:

- NCS accounts payable, fixed assets, inventory, time entry, work orders, and general ledger

- Accounts receivable, cash receipting, bank management and rates, plus inputs from other Local Government regulatory systems such as Person/Property, Infringements, Licensing, Consents.

Monthly and yearly expenditure reporting is presented to Council staff, Council representatives and Scheme Committees and identifies current concerns and trends.

11.7 Improvement Plan

Throughout this section a number of specific actions to improve the way in which the Council manages its financial forecasting and funding associated with the 5Waters activities. These actions are summarised below in Table 11‑7.

Table 11‑7 AM Improvement Items – Financial Summary

| 11.2.1 | Consolidate rates to ensure financial sustainability | High | Ongoing |

| 11.2.1 | Integrate schemes where economically viable | Medium | Ongoing |

| 11.5 | Implement a form of budget editing software | Medium | 2020/21 |

| 11.5 | Use the budget editing module for 2021-31 LTP | Medium | 2020/21

|

<<

5-Waters Volume 1